Customs

Is your company involved in triangular sales? Discover the rules that apply to triangular transactions:

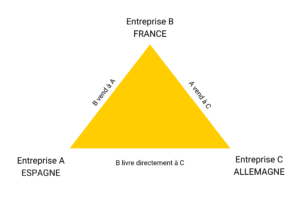

A triangular operation occurs when 3 separate companies, located in 3 different EU member states, are involved in the same physical flow of goods.

For example, a French company A may buy goods from a Spanish supplier B for resale to a German customer C. In this triangular operation, which is very common in industry, the company in France is considered to be an “intercalary” or “buyer/seller” company, since the goods are exported directly from Spain (supplier) to Germany (customer).

The Directive of December 16, 1991, simplified by the European Commission in 1992, stipulates that company B, the so-called “intercalary” company, cannot avoid value-added tax on triangular transactions: it is liable for VAT on triangular transactions.

However, a number of simplification measures have been introduced, framed and clarified as the VAT Directives have evolved.

In our example of a triangular operation, French company B would have to identify itself in either Spain or Germany.

A VAT expert to help you declare your sales, simplify your procedures and save time:

Make an appointment

Here are the basic rules for triangular operations:

What if B is not identified for VAT purposes in either of the two member states? Article 141 of Directive 2006/112/EC of November 28, 2006 provides for simplified taxation of triangular transactions. Thanks to this directive, the intercalary company can avoid value-added tax on triangular transactions.

However, for these measures to be applicable, the 3 companies involved in the triangular operation must each be identified in their respective countries, and the buyer/seller company must not be identified in the country of departure and/or destination of the goods.

The simplification also applies when, in a triangular operation, the intercalary company is a non-EU company identified in a Member State that is neither the place of departure nor the place of delivery of the goods.

Would you like to know more about taxation on the transport and export of goods in a triangular operation? Fiscalead’s experts are on hand to explain everything you need to know about your obligations during a triangular operation: find out more about our services if you are subject to VAT.